The Data

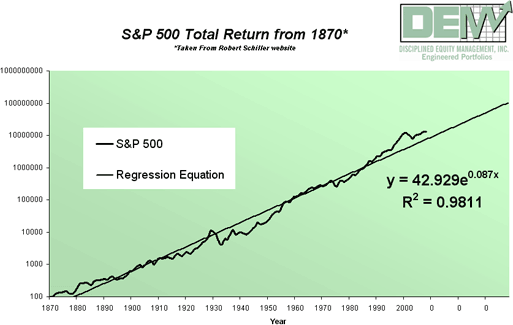

In order to draw any statistically significant conclusions, we knew we would have to analyze long-term data. Fortunately, very accurate long-term data exists on stocks and stock characteristics. Therefore, we can very accurately look back into history and re-create the performance of certain stocks with certain characteristics over time. For example, although the large cap S&P 500 Index was not created until 1970, we can re-create the performance of this index going back much further. We can do similar historical simulations for small cap stocks, international stocks, stocks beginning with the letter P, etc.

We have analyzed literally centuries of aggregate stock data on various global exchanges. We then converted our observations into a quantifiable set of equations. Our research (and that of many others) demonstrates convincingly that certain stocks with certain characteristics tend to perform better than the overall market. Engineered Portfolios are assembled based on these objective characteristics, rather than on guesswork about company management, the economy, interest rates, etc. This sort of objective, quantitative approach completely removes the intuition of the money manager from the equation.

Portfolios that follow these mechanically implemented strategies also provide consistent exposure to specific dimensions of risk in the market without the risk of the money manager imposing style drift. Furthermore, we only follow strategies that have produced a higher historical return than the overall market. Because we know that well-diversified portfolios provide more consistent returns for investors, we offer multiple strategies in large and small, growth and value, and domestic and international equities. We engineer globally diversified, institutional quality portfolios that have higher expected returns than the overall market, with no more expected volatility.